Zeta Global Holdings (ZETA)·Q4 2025 Earnings Summary

Zeta Global Delivers 18th Consecutive Beat & Raise, Stock Surges 13%

February 24, 2026 · by Fintool AI Agent

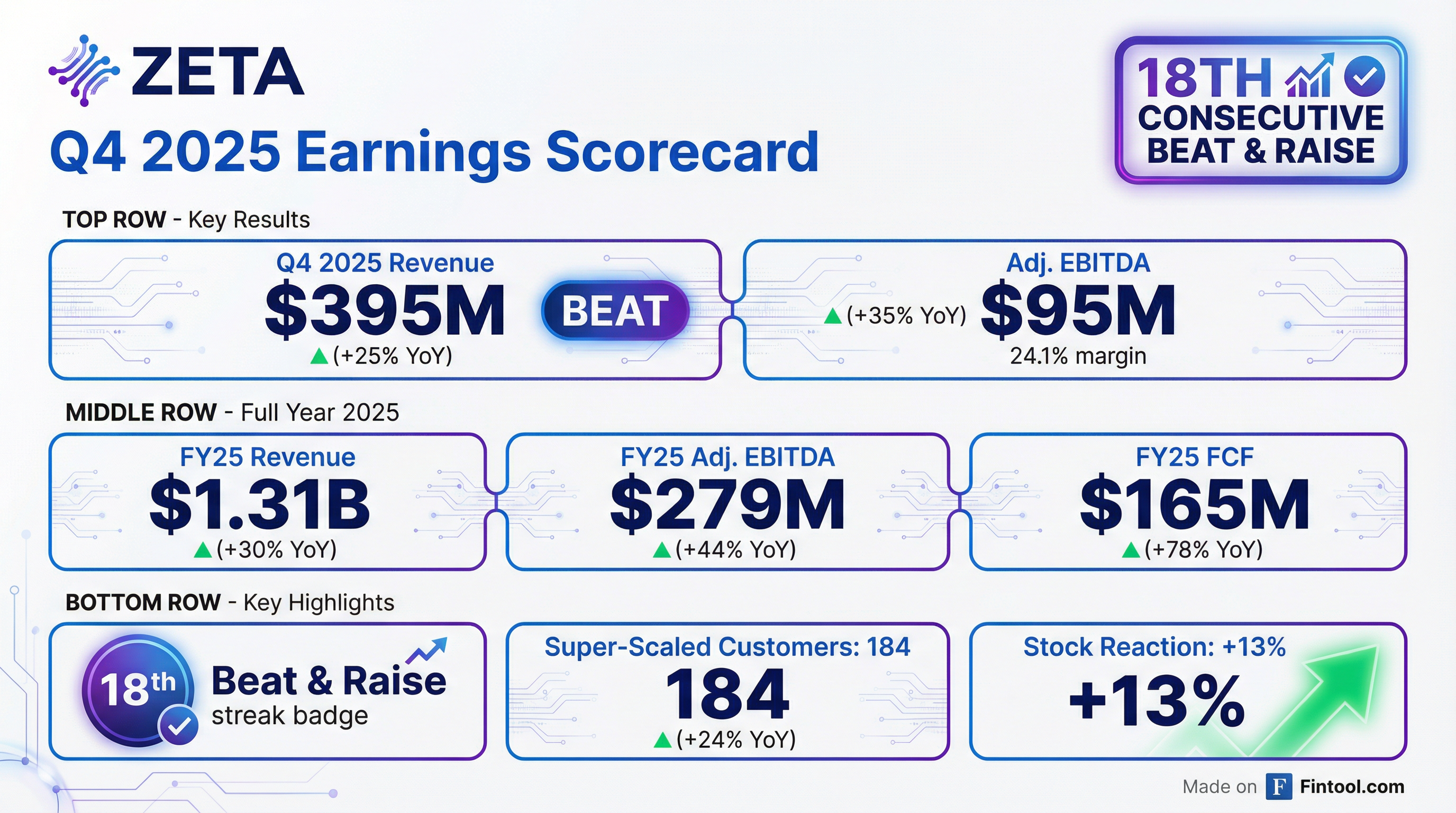

Zeta Global (NYSE: ZETA) reported its 18th consecutive beat-and-raise quarter, delivering Q4 2025 revenue of $395M that topped guidance by $14M (+3.7%). The AI marketing cloud company raised full-year 2026 guidance across all metrics and announced it expects to achieve GAAP profitability in FY26—a significant milestone for the growth stock. Shares jumped 13% to $16.98 on the results.

Did Zeta Beat Earnings?

Yes—decisively. Zeta beat on revenue, profitability, and cash flow while extending its remarkable streak.

Full Year 2025 Highlights:

- Revenue: $1.305B (+30% Y/Y)

- Adj. EBITDA: $279M (+44% Y/Y), 21.4% margin (+217 bps)

- FCF: $165M (+78% Y/Y), 59% conversion, 13% margin

CEO David Steinberg attributed the results to "the compounding power of our system: proprietary data that improves with every customer interaction, intelligence that sharpens with every decision, and now Athena by Zeta—an interface that lowers the barriers to enterprise-wide adoption."

What Did Management Guide?

FY26 guidance raised across the board, with a major milestone: GAAP profitability.

Q1 2026 Guidance:

- Revenue: $369-371M (+39-40% Y/Y)

- Adj. EBITDA: $61.2-61.8M (+31-32% Y/Y), 16.6% margin

Zeta 2028 Targets Raised:

Zeta updated its medium-term targets to reflect the Marigold Enterprise Business acquisition:

CFO Chris Greiner noted: "We see 2026 as another year in which total revenue growth can eclipse 30% while simultaneously turning GAAP Net Income positive, a significant milestone for the company."

What Changed From Last Quarter?

Customer Metrics Accelerating

Key Observations:

- ~90% of FY25 revenue came from customers with Zeta for >1 year

- Customers >5 years generate $3.9M ARPU vs. $0.7M for <1 year cohort

- Super-scaled customers approaching ~90% of total revenue

Vertical Diversification

9 of Zeta's top 10 verticals grew >20% Y/Y in FY25. Top 5 fastest growing:

- Travel & Hospitality

- Advertising & Marketing

- Automotive

- Consumer & Retail

- Telecom

Zeta now serves 51% of the Fortune 100, including:

- 12 of 15 largest Consumer & Retail companies

- 4 of 4 largest Telecommunications companies

- 10 of 13 largest Technology & Media companies

How Did the Stock React?

Zeta surged 13% to $16.98 on earnings day, though shares remain well below the 52-week high of $24.90.

The strong reaction reflects:

- 18th consecutive beat-and-raise quarter (unprecedented consistency)

- Path to GAAP profitability in FY26

- Raised 2028 targets

- Accelerating customer additions (+24% super-scaled growth)

Key Financial Trends (8 Quarters)

16 consecutive quarters of >20% revenue growth.

Adj. EBITDA Margin Progression:

- FY22: 15.6% → FY23: 17.8% → FY24: 19.2% → FY25: 21.4%

- 20 consecutive quarters of expanding Adj. EBITDA margins Y/Y

Capital Allocation & Balance Sheet

Zeta repurchased $121M of stock in FY25 while maintaining a net cash position. The company has demonstrated disciplined capital allocation between organic investment, M&A (LiveIntent, Marigold Enterprise Business), and buybacks.

What's Driving Growth?

The "One Zeta" Platform Flywheel

Zeta's thesis centers on converging identity data, AI intelligence, and omnichannel activation into a single platform:

- Proprietary Data Asset - 245M US individuals permissioned for online tracking, 110M for email

- AI Intelligence - Athena by Zeta interface lowering barriers to enterprise adoption

- Omnichannel Convergence - Customers using 3+ channels generate ~17x more revenue than single-channel

Recognition

Zeta was named the Leader in Forrester Wave for Email Marketing Service Providers (3Q 2024), scoring highest possible rating in 13 of 22 categories.

Risks and Concerns

- Marigold Integration - Recently acquired Enterprise Business adds ~$190M revenue but execution risk remains

- Political Revenue Volatility - Political candidate revenue was $44M in FY24 but "not material" in FY25

- Stock-Based Compensation - $178M in FY25 (14% of revenue), though declining from $195M in FY24

- Customer Concentration Risk - Top customers represent meaningful revenue (though diversifying)

- Macro Sensitivity - Marketing spend correlates with economic cycles

Forward Catalysts

- Q1 2026 Results (May 2026): First quarter reflecting full Marigold contribution

- GAAP Profitability - Expected in FY26, would be first profitable year

- Zeta 2028 Progress - Tracking toward $2.3B revenue, $573M EBITDA targets

- AI Product Expansion - Athena platform adoption curve

- Direct Mix Expansion - Currently 74%, target 70-75% range

Bottom Line

Zeta delivered another flawless quarter—its 18th consecutive beat-and-raise—while raising guidance and announcing a path to GAAP profitability. The customer metrics tell the story: super-scaled customers up 24%, 9 of 10 verticals growing >20%, and ARPU expanding as customers adopt more channels. With FY26 guidance calling for 35% revenue growth and GAAP profitability, Zeta continues to prove it can deliver "durable, predictable, and profitable growth at scale."

Related Links: